UK House Prices Forecast 2026–2030

The UK property market stands at a pivotal point in 2026, following several years of economic uncertainty, interest rate fluctuations, and shifting buyer behavior. After a period of volatility driven by pandemic demand, rising living costs, and tighter borrowing conditions, the market is now moving towards a more stable and predictable phase. Looking ahead to 2030, expectations center on gradual recovery, modest price growth, and improving confidence among both buyers and investors.

For those searching for houses for sale or evaluating rental options, understanding house price forecasts and market trends is essential. Property decisions are long-term commitments, and even small changes in mortgage rates, affordability, or regional demand can significantly impact outcomes. A well-informed approach helps buyers and investors make confident choices rather than reacting to short-term uncertainty.

Table of Contents

The Current State of the UK Housing Market

As we move through 2026, the UK housing market has achieved a degree of stability that many observers welcome after previous turbulence. Average house prices across the country are currently in the region of £268,000 to £290,000, depending on the specific index and location. Recent annual growth has been modest, typically between 1% and 2.5% in many areas, reflecting a more balanced environment where supply and demand are closer to equilibrium than in previous boom periods.

This stabilisation comes after several years of adjustment. Higher borrowing costs had cooled buyer activity, but as inflation has moderated and the Bank of England base rate has eased towards 3.75%, mortgage rates have become more manageable for many households. Fixed-rate deals in the mid-4% range are now commonly available for borrowers with reasonable deposits and credit profiles.

Importantly, the chronic shortage of housing continues to act as a strong underlying support for prices. Successive governments have set ambitious targets for new home construction, but delivery has consistently fallen short due to planning delays, labour shortages, and economic viability issues for developers. This persistent undersupply means that demand for quality houses for sale in desirable locations often exceeds what is available, preventing any significant price corrections even when economic headwinds appear.

Northern regions, including Yorkshire and the Humber, have performed relatively well compared to the more expensive southern markets. Cities such as Leeds and Bradford continue to attract interest from buyers seeking better value, strong employment prospects, and ongoing regeneration projects. This north-south divide is expected to remain a defining feature of the market through the rest of the decade.

Detailed UK House Price Forecast for 2026–2030

Leading property consultancies and economic forecasters present a broadly consistent picture for the coming five years. Growth is expected to start modestly in 2026 before accelerating as affordability improves and economic conditions stabilise.

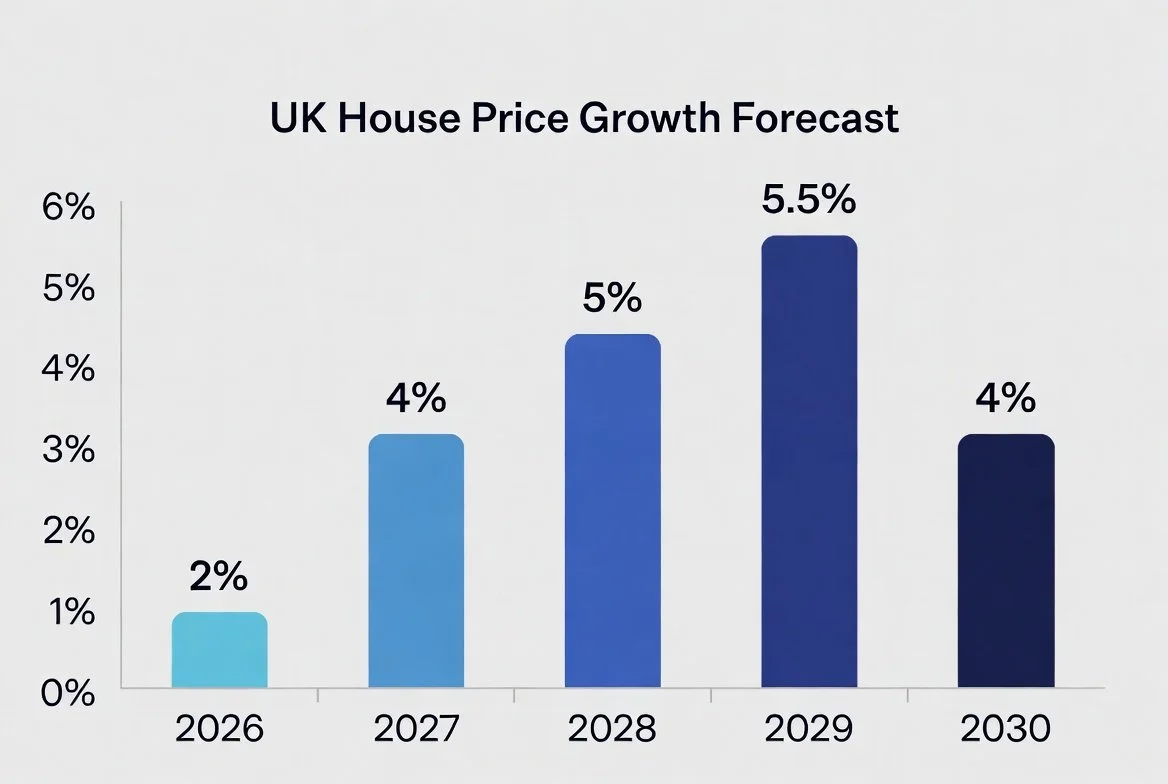

Savills, one of the most respected sources for long-term forecasts, projects national house price growth of approximately 2% in 2026, rising to 4% in 2027, 5% in 2028, 5.5% in 2029, and 4% in 2030. This pathway suggests cumulative growth of around 22% over the full period, delivering meaningful appreciation for those who enter the market at the right time. Other major forecasters broadly align with this view. Knight Frank anticipates slightly more conservative figures in the early years but expects momentum to build towards the end of the decade. The Office for Budget Responsibility (OBR) models average annual growth close to 2.5–3.5% when aligned with expected earnings growth. Nationwide and Rightmove data also support the idea of a gradual strengthening market rather than dramatic swings.

This trajectory represents a healthy normalisation rather than the exceptional gains seen during ultra-low interest rate periods. For buyers searching for houses for sale today, it suggests that entering the market in 2026 could allow them to benefit from the stronger growth expected in subsequent years.

Regional House Price Outlook Across the UK

One of the most important aspects of the 2026–2030 forecast is the significant variation between regions. Northern and Midlands markets are widely tipped to outperform London and the South East due to better affordability, ongoing investment, and internal migration patterns.

Yorkshire and the Humber stand out as areas with particularly positive prospects. Average prices in West Yorkshire remain noticeably below the national average, offering more accessible entry points for families and first-time buyers. Leeds benefits from its status as a major financial and tech centre, while Bradford continues to see regeneration that enhances its appeal. Forecasters expect cumulative growth in these northern regions to reach 27–30% over the five years in optimistic scenarios.

These regional differences create meaningful opportunities. Buyers who might struggle to afford property in southern England often find greater choice and value when exploring houses in Yorkshire and surrounding areas. The combination of lower purchase prices and solid long-term growth potential makes these locations attractive for both owner-occupiers and those looking at properties for rent as investments.

Mortgage Rates And and Borrowing Conditions

Mortgage availability and cost will play a crucial role in determining how the forecast unfolds. In 2026, competitive fixed-rate mortgages are available in the mid-4% range for borrowers with deposits of 10-25% or more. Further gradual easing of the Bank of England base rate could bring average rates down modestly over the next few years, significantly improving monthly payments for many households.

Wage growth that outpaces house price increases in the early part of the forecast period will help restore affordability. However, larger deposits and strict stress-testing requirements mean that saving remains important for first-time buyers. Those who can secure finance now may benefit from locking in relatively attractive rates before stronger market momentum potentially pushes prices higher later in the decade.

Lenders have adapted to the current environment with more products tailored to different buyer types, including support for professionals in growing regional cities. Independent mortgage advice is highly recommended to understand the full range of options available.

Housing Supply Challenges and Government Policy

The single biggest long-term driver of UK house prices remains the gap between housing supply and demand. Despite repeated pledges to build hundreds of thousands of new homes annually, actual delivery continues to lag. This structural imbalance is expected to persist through 2030, providing ongoing support for values in most areas.

Policy changes also influence the market. Reforms to the rental sector have encouraged some landlords to sell properties for rent, increasing stock available for owner-occupiers in certain locations. Stamp duty adjustments affect transaction costs, particularly for higher-value homes or additional properties. Planning system changes aim to speed up development, but local opposition and infrastructure requirements often slow progress.

For buyers, these factors mean that well-located existing properties in established areas will likely hold their value strongly, while new-build opportunities may offer incentives but come with their own considerations around quality and service charges.

Rental Market Forecast and Properties for Rent

The private rental sector remains extremely relevant to the overall housing picture. Limited supply, combined with some landlords reducing their portfolios due to regulatory changes, is expected to keep rental growth strong at 4–6% per year in many regional markets through 2030.

This environment benefits both tenants seeking stability and landlords looking for properties for rent that deliver reliable income alongside capital growth. In high-demand areas such as Leeds, professional tenants create consistent demand for well-maintained family homes and apartments. Yields may moderate slightly as purchase prices rise, but total returns from rental income plus appreciation remain compelling in affordable northern locations compared to southern markets.

For tenants, rising rents strengthen the long-term financial case for buying when personal circumstances allow. The interplay between sales and rental markets will continue to be a key feature of the UK housing landscape.

Key Risks and Factors That Could Alter the Outlook

While the baseline forecast is positive, several risks could influence actual outcomes. Geopolitical events, unexpected inflation spikes, or slower-than-expected economic growth could delay rate cuts and dampen buyer confidence. Changes in government policy or significant shifts in migration patterns might also affect regional performance.

Conversely, faster progress on housebuilding or sharper falls in borrowing costs could moderate price growth in some areas. Buyers and investors should maintain realistic expectations and build flexibility into their plans. Diversifying across locations or property types can help manage risks effectively.

Practical Advice for Potential Buyers

Those actively looking at houses for sale in 2026 should focus on preparation and thorough research. Obtaining a mortgage agreement in principle early demonstrates seriousness to sellers and clarifies realistic budgets. Working with experienced local agents and professionals helps identify properties that match both current needs and future growth potential.

Key considerations include location fundamentals such as transport links, schools, employment opportunities, and planned infrastructure improvements. Professional surveys and legal checks remain essential to avoid unexpected costs. Budgeting for stamp duty, legal fees, moving expenses, and ongoing maintenance provides a more accurate picture of total commitment.

For investors, selecting properties for rent requires careful analysis of tenant demand, void periods, and management costs. A medium to long-term approach aligns best with the forecasted growth trajectory.

Historical Trends in UK Property Value

Looking back, UK house prices have shown remarkable resilience over decades despite periodic corrections. Supply shortages, population growth, and economic expansion have consistently driven values higher over the long term. The 2026–2030 period fits within this broader pattern a phase of recovery and normalisation that rewards patient, well-informed participants.

Property continues to serve as a primary vehicle for wealth building for millions of British households. When chosen carefully and held over time, it provides both a home and a hedge against inflation.

Opportunities in the UK Property Market 2026–2030

HMOs carry higher regulatory responsibilities and are subject to stricter enforcement. Landlords must maintain valid licences, enhanced fire safety systems, and safe communal areas. Regular inspections, proper waste management, and compliance with room size and occupancy standards are essential to ensure tenant safety and meet local authority housing regulations consistently.

Essential HMO Standards & Compliance

Valid HMO licence

Fire safety upgrades and systems

Regular inspections of shared areas

Proper waste management systems

Compliance with room size regulations

HMOs are subject to higher enforcement scrutiny.

Conclusion

The house price forecast for 2026–2030 presents a balanced yet promising picture. Modest growth in the near term gives way to stronger appreciation later in the decade, supported by fundamental supply constraints and improving affordability. Regional variations offer particularly attractive prospects in northern England, including Yorkshire, for those seeking value and growth potential.

Whether you are buying your family home or building a portfolio of properties for rent, success depends on thorough research, professional advice, and alignment with your personal financial circumstances and timeline. The market is not without risks, but for prepared buyers with a suitable horizon, the coming years could deliver solid returns and the security that property ownership provides.

Markets will continue to evolve, so staying informed and flexible remains important. By understanding the detailed forecasts and regional dynamics outlined here, you can approach decisions about houses for sale with greater confidence.

FAQs

What is the UK house price forecast for 2026–2030?

Most forecasts suggest steady, moderate growth over this period, with overall prices expected to rise gradually rather than sharply. Cumulative growth is commonly estimated in the range of 15% to 25% by 2030, depending on economic conditions and regional performance.

Will UK house prices crash during 2026–2030?

A major crash is not widely predicted. Instead, the market is expected to remain relatively stable, with short-term fluctuations but no sustained national decline. Structural housing shortages continue to support long-term price stability.

Which regions are expected to grow the most?

Northern England, the Midlands, Scotland, and parts of Wales are expected to outperform due to affordability, regeneration projects, and stronger rental demand. Cities such as Leeds and Bradford are often highlighted for value-driven growth potential.

Are London and the South East still good investments?

London and the South East are expected to see slower growth compared to other regions, mainly due to affordability limits. However, they may still offer long-term stability and strong rental demand, especially in well-connected areas.

How will mortgage rates affect the market?

Mortgage rates are expected to gradually ease over time, improving affordability and buyer confidence. However, they are unlikely to return to the ultra-low levels seen in previous years, meaning growth will remain measured.

Is 2026–2030 a good time to buy property in the UK?

For many buyers, this period offers a more balanced and predictable market. It is generally favourable for long-term buyers and investors focused on steady growth and rental income rather than short-term gains.

Thinking about buying or investing based on UK house price forecasts? Get in touch with Armaani Estates today.