Is 2026 a Good Year to Buy Property in the UK?

As we move through 2026, one of the key questions for buyers, investors, and homeowners alike is whether this year truly presents a favourable opportunity to enter or expand within the UK property market. Following several years of uncertainty shaped by pandemic era price surges, persistent inflation, and fluctuating interest rates the housing sector has now transitioned into a phase of cautious and controlled stability.

Rather than the dramatic highs and lows seen in recent years, house prices are now experiencing modest and more sustainable growth. This shift reflects a rebalancing of supply and demand, alongside improved market predictability. For buyers, this environment offers selective opportunities, particularly for those who are financially prepared and focused on long-term value rather than short-term gains.

At the same time, expectations need to remain grounded, as rapid capital appreciation is no longer the norm. This comprehensive guide explores the UK property market in 2026 in detail, helping you understand key trends, risks, and opportunities to make a confident and informed decision.

Table of Contents

UK Property Market 2026

The UK property market in 2026 is shaped by a mix of stabilising house prices, improving mortgage conditions, and continued regional variation. After a period of uncertainty, the market is showing signs of balance, with moderate price growth expected in many areas. While affordability remains a key concern, easing interest rates are helping to restore buyer confidence.

Regional markets, particularly in the North of England and Yorkshire, continue to attract attention due to their relative affordability and stronger growth potential compared to the South. At the same time, demand remains steady across different buyer groups, including first-time buyers, families, and investors. Understanding these market conditions is essential for anyone considering a property purchase in 2026, helping to make informed and well-timed decisions.

Current State of the UK Housing Market in 2026

As of early 2026, the average UK house price sits around £268,000 to £271,500, reflecting modest annual growth of approximately 1.3% in recent official data. The market has demonstrated remarkable resilience, with transaction volumes holding steady near pre-pandemic averages in many areas despite higher borrowing costs compared to the ultra-low rate era.

Economic conditions play a central role. Inflation has moderated but remains sensitive to global events, particularly tensions in the Middle East affecting energy prices. The Bank of England base rate has eased to around 3.75%, with mortgage rates for typical fixed deals hovering in the mid-4% range. While not as cheap as a few years ago, these levels represent an improvement from 2023 peaks and support gradual recovery in buyer activity.

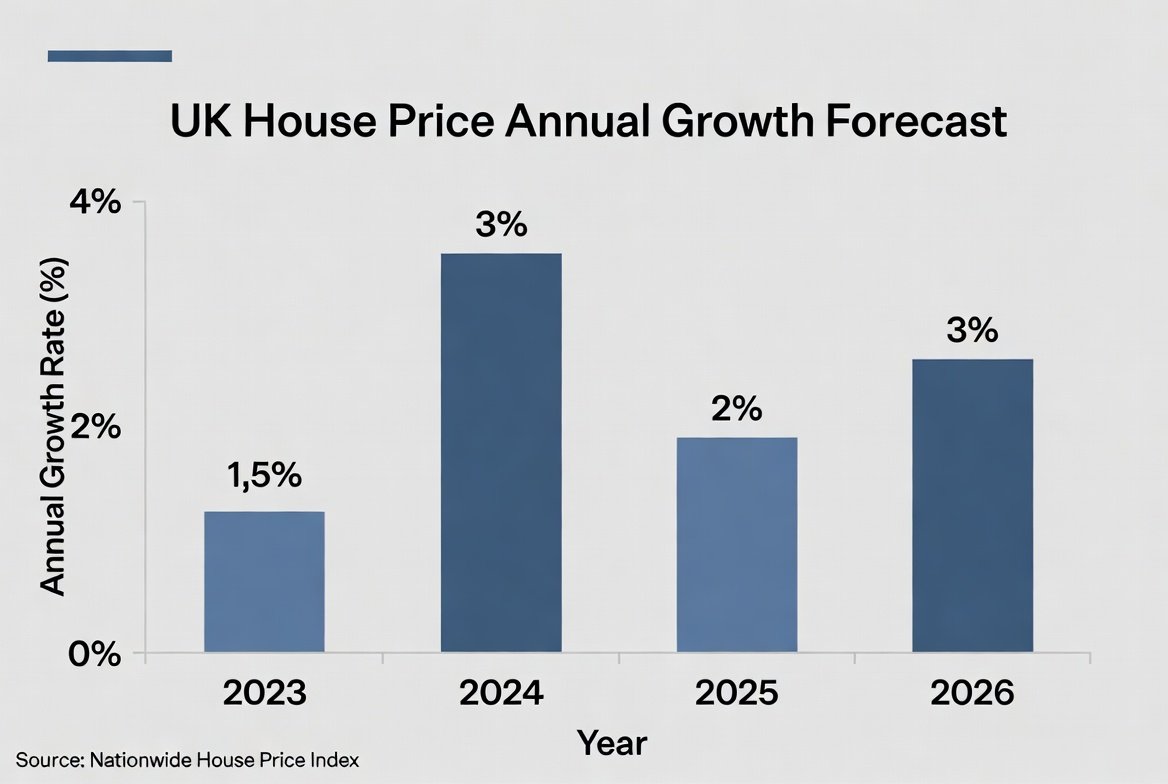

2026 House Price Forecasts: Expert View

Consensus among major forecasters points to modest national house price growth in 2026, typically in the 2% to 4% range.

Nationwide Building Society expects growth between 2% and 4%, driven by improving affordability as wage growth outpaces property price rises. Savills and Rightmove forecast around 2%, while Halifax anticipates 1% to 3%. These projections reflect a balanced market where neither buyers nor sellers hold overwhelming power.

Longer-term outlooks remain more positive. Many analysts project stronger cumulative growth from 2027 onwards as economic conditions stabilise and mortgage rates potentially ease further. However, near-term gains will likely remain steady rather than spectacular, rewarding those with a five-to-ten-year horizon over short-term speculators.

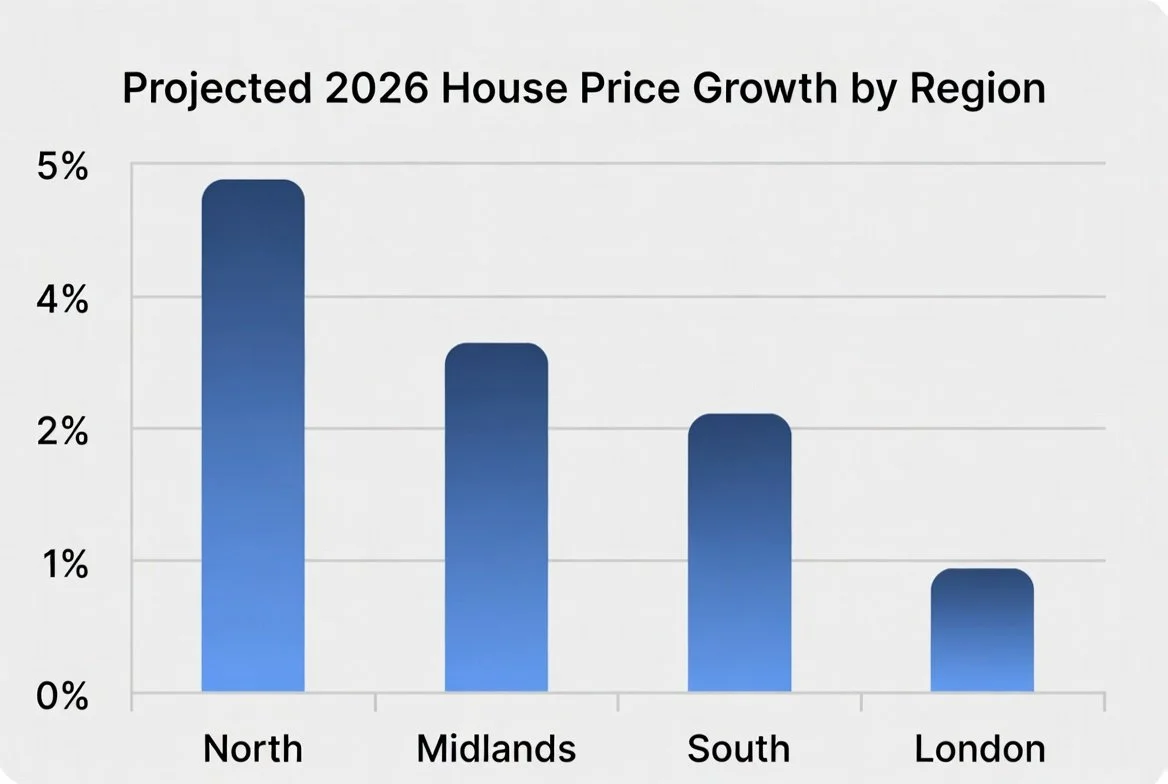

Why the North and Yorkshire Stand Out

Buyers seeking better value and growth potential are increasingly looking beyond southern hotspots. Yorkshire and the Humber, including key cities like Leeds and Bradford, frequently feature in forecasts as areas with stronger relative performance.

West Yorkshire property prices average significantly below the national figure, often around £240,000, offering more accessible entry points for families and first-time buyers . Local forecasts suggest 3% to 5% growth potential in 2026, supported by ongoing regeneration projects, strong employment in sectors like finance, tech, and manufacturing in Leeds, and improving transport links.

Bradford benefits from characterful Victorian housing stock, investment in city centre areas, and relative affordability that attracts both owner-occupiers and investors. Leeds continues to draw professionals with its economic dynamism, creating consistent demand for family homes and apartments. These factors combine to create a more buyer-friendly environment compared to overheated southern markets, where price growth may remain subdued at 1-2%.

Other strong performers include parts of the North West and Midlands, where similar dynamics of affordability and regeneration play out. In contrast, prime central London faces headwinds from higher taxes and global uncertainty, leading to flatter performance in many segments.

Mortgage Rates and Affordability Landscape

Mortgage affordability has improved gradually but remains a key consideration. Average rates for 2- and 5-year fixed deals have stabilised after earlier volatility, with competitive deals available for those with solid deposits and credit profiles. Lenders report healthy competition, which helps keep options available for buyers.

Wage growth continuing to outpace modest house price increases helps many households. However, larger deposits (typically 10-20% or more) and rigorous stress-testing still present barriers, particularly for first-time buyers without family support. Those who can secure a mortgage in 2026 benefit from greater payment certainty compared to variable-rate borrowers in previous volatile periods.

Independent advice is essential. Tools like mortgage calculators and broker consultations can reveal realistic budgets, factoring in future rate expectations and personal circumstances.

Policy Changes and Their Impact on Buyers

Government policy continues to play a significant role in shaping the UK property market. Stamp Duty Land Tax (SDLT) rules mean that many buyers are taxed on portions of a property’s value above £125,000, with additional surcharges applying to second homes and investment properties. While first-time buyer relief offers some assistance, its impact is limited, particularly in mid-range price brackets where upfront costs remain a key barrier.

Recent rental reforms, including the Renters’ Rights Act, alongside broader landlord-focused regulations, have encouraged some investors to reassess or exit the market. This has, in certain areas, contributed to a modest increase in available housing stock, particularly in rental-heavy regions.

At the same time, planning reforms are intended to support long-term housing supply, although actual delivery continues to face structural challenges such as local constraints and development delays. Overall, these policies are creating a more regulated and cautious market environment, without fundamentally reducing underlying demand driven by population growth and ongoing housing shortages.

Advantages of Buying Property in 2026

Several factors make 2026 potentially attractive for many prospective buyers. Modest price growth means entering the market now could secure a property before values rise further over the coming years. In segments with higher stock levels, buyers often have greater negotiating power on price, inclusions, or repairs, a welcome shift from seller-dominated periods.

Long-term property ownership builds equity and provides stability against rental increases, which continue to rise due to supply constraints in the private rented sector. For those planning to stay in an area for five years or more, the combination of potential capital appreciation and the security of homeownership often outweighs the costs of renting, especially as mortgage payments contribute to building personal wealth rather than a landlord’s equity. Regional markets with strong fundamentals, such as those in Yorkshire, offer particularly compelling value propositions, combining lower entry prices with solid rental demand and economic prospects.

Investors may find opportunities in buy-to-let where tenant demand remains robust, though careful selection of location and property type is crucial for sustainable yields.

Potential Drawbacks and Risks to Consider

No market analysis would be complete without acknowledging challenges. Absolute price levels remain high by historical standards, and when combined with mortgage costs and transaction expenses (legal fees, surveys, moving), the total outlay can feel substantial. Economic uncertainties, including geopolitical risks, potential slowdowns in growth, or shifts in employment, could pressure prices or buyer confidence in the short term.

Interest rate volatility remains a factor. While forecasts suggest relative stability, unexpected inflation spikes could delay further easing. Those with shorter time horizons or stretched finances may find renting allows greater flexibility while building savings.

Maintenance, energy efficiency upgrades, and council tax add ongoing costs that renters typically avoid. Liquidity can also be an issue; selling quickly in a balanced market may require realistic pricing rather than achieving maximum value immediately.

Timing the market perfectly is notoriously difficult. Waiting for significant price drops has often proven costly, as genuine crashes are rare and recoveries can be swift once conditions improve.

First-Time Buyers, Families, and Investors

First-time buyers face a mixed but navigable environment. Improved stock levels in some areas and potential negotiation room help, though saving for deposits remains the biggest hurdle. Government schemes and shared ownership options can bridge gaps in suitable developments. Focusing on affordable regions with good transport and amenities often yields the best outcomes.

Families prioritising space, schools, and community benefit from exploring suburban and regional options where properties offer more for the money. Areas undergoing regeneration frequently provide modern family homes at competitive prices relative to established hotspots.

Investors should adopt a long-term mindset. Rental demand supports yields in high-employment cities, but increased regulation and tax changes compress margins compared to previous decades. Successful strategies focus on properties with strong tenant appeal, low void periods, and locations with sustained economic drivers rather than chasing high short-term capital gains.

Practical Steps for Buyers in 2026

Successful purchasing begins with thorough preparation. Obtain a mortgage agreement in principle early to understand realistic budgets and strengthen your position with sellers. Budget for all associated costs, including a contingency of 5-10% for unexpected expenses.

Research remains vital. Examine local market trends using official indices, visit areas at different times, and assess factors like transport links, schools, flood risk, and future development plans. Professional surveys provide essential peace of mind beyond basic valuations.

Work with experienced local professionals who understand micro-market dynamics. Compare multiple properties and be prepared to negotiate based on survey findings or market conditions. Consider the full lifecycle of ownership: energy performance, potential extension possibilities, and alignment with personal or family needs over the next decade.

Historical Context and Long-Term Outlook

UK property has historically delivered strong long-term returns, even through multiple economic cycles. From post-war levels to today’s market, sustained price growth has been driven by structural factors such as chronic housing undersupply, steady population growth, and long-term economic expansion. While inflation-adjusted gains are more moderate, they remain consistently positive for those holding property over extended periods.

The year 2026 represents a period of normalisation, as the market moves away from the distortions created by years of ultra-low interest rates toward more balanced and sustainable conditions. Despite this shift, the fundamental drivers of UK house price growth remain firmly in place.

As a result, well-selected properties in strong, high-demand locations continue to act as both a long-term store of value and a wealth-building asset for many households, particularly for those focused on stability rather than short-term speculation.

Rental Market Impact on Buying Decisions

The private rental sector continues to face significant structural pressures, with rents rising steadily due to persistent supply shortages and a gradual reduction in the number of active landlords. As some property owners exit the market or consolidate their portfolios in response to regulatory changes and cost pressures, competition for available rental homes has intensified, further driving upward pressure on prices.

In this context, homeownership is becoming increasingly attractive for those able to make the transition. While mortgage payments require a higher initial commitment, they contribute directly toward building long-term equity in an asset, rather than being spent entirely on rent with no financial return. Over time, this shift can create a clearer pathway to financial stability and wealth accumulation compared to long-term renting.

At the same time, strong and sustained rental demand continues to present opportunities for investors in the buy-to-let sector. This is particularly evident in university cities, major employment hubs, and well-established family-oriented residential areas, where tenant demand remains consistently high. In such locations, limited housing supply combined with stable demand helps support rental yields and occupancy rates, making carefully selected investment properties potentially resilient even within a tightening regulatory and market environment.

Key Risks and How to Mitigate Them

Global events, policy shifts, and broader economic slowdowns all have the potential to reshape market trajectories in unexpected ways. As a result, building financial resilience is essential. Diversifying personal finances, maintaining a well-funded emergency reserve, and selecting properties with strong, long-term appeal can all help mitigate downside risks in uncertain conditions. Equally important is conducting thorough due diligence before committing to any purchase, alongside seeking professional advice where necessary, as this significantly reduces the likelihood of unforeseen costs or complications arising later.

In addition to financial and market risks, climate considerations and evolving energy efficiency standards are becoming increasingly central to property decisions. Homes that do not meet modern efficiency expectations may require substantial upgrades in the future, which can impact overall affordability and returns. For this reason, it is increasingly sensible for buyers to factor potential retrofit or improvement costs into their initial purchase calculations. Prioritising well-insulated, energy-efficient properties not only supports long-term cost savings but also helps safeguard future resale value as regulations and buyer expectations continue to evolve.

Making the Right Decision for Your Circumstances

Is 2026 a good year to buy property in the UK? For many people, particularly those financially prepared, focused on suitable locations, and committed to a medium-to-long-term horizon, the answer is yes. The market offers a more balanced environment with buyer opportunities, modest growth potential, and structural supports that have historically favoured owners.

However, it is not universally ideal. Individuals with tight budgets, short timeframes, or significant uncertainty in their personal situation may benefit from continuing to rent while strengthening their position.

Ultimately, property decisions are deeply personal. They depend on your income stability, family needs, risk tolerance, and local market conditions. Conduct detailed research, seek independent financial and legal advice, and focus on properties that meet your lifestyle requirements rather than chasing headlines.

In a market characterised by steady rather than sensational movement, informed and patient participants tend to achieve the best long-term results. Whether you are taking your first step onto the ladder or expanding your portfolio, 2026 presents a window of relative stability worth serious consideration.

FAQs

Is 2026 a good time to buy property in the UK?

2026 is generally viewed as a more balanced and stable housing market, offering improved price predictability and better negotiating conditions compared to the volatility of recent years. It is often more suitable for long-term buyers who are financially prepared and focused on steady growth rather than short-term gains.

Will UK house prices fall in 2026?

Most forecasts indicate that house prices are likely to remain broadly stable, with modest growth rather than a significant decline. Any changes are expected to stay within a low single-digit range nationally, although performance will still vary between regions and property types.

Which regions offer the best opportunities in 2026?

Northern England and parts of the Midlands are widely considered stronger opportunity areas due to affordability, regeneration projects, and sustained demand. Cities across Yorkshire, including Leeds and Bradford, often stand out for value, rental demand, and long-term growth potential.

How are mortgage rates affecting affordability?

Mortgage rates have stabilised compared to previous peaks, with many fixed-rate deals typically sitting in the mid-4% range. While this is higher than historic lows, improving wage levels and increased competition among lenders are helping to support overall affordability.

Is it better to buy or continue renting in 2026?

Buying tends to suit those planning to stay in one location long term, as it allows equity growth and protection from rising rental costs. Renting may still be more appropriate for individuals who need flexibility or are uncertain about their long-term financial or location plans.

What are the main risks of buying property in 2026?

Key risks include ongoing economic uncertainty, potential interest rate fluctuations, high upfront costs such as deposits and fees, and uneven regional performance. Careful financial planning, thorough research, and professional advice are important to manage these risks effectively.